Section threeFood and Land Use

Introduction

The global food and land use system is at a pivotal moment. Continuing down our current path will undermine the world’s ecological foundations. It will also contribute significantly to a series of challenges, including rural poverty, social conflict, hunger, obesity, malnutrition, biodiversity loss, soil erosion, and climate change. Fix it, however – based on tried and tested policy reforms, better agricultural techniques and financial instruments, and the innovations these measures are sure to catalyse – and our food and land use system could instead provide stronger and more equitable rural socioeconomic development, deliver over one-third of the climate change solution,1 keep secure our vital biodiversity, and generate massive improvements in public health. There is a clear economic case for fixing this broken system: Recent analysis has shown that developing sustainable food and land use-business models could be worth up to US$2.3 trillion and provide over 70 million jobs by 2030.2 In short, the transition to sustainable food and land use systems represents an opportunity that no country, nor indeed the world, can afford to ignore. Not making the transition, meanwhile, entails risks and costs that no responsible leader should accept.

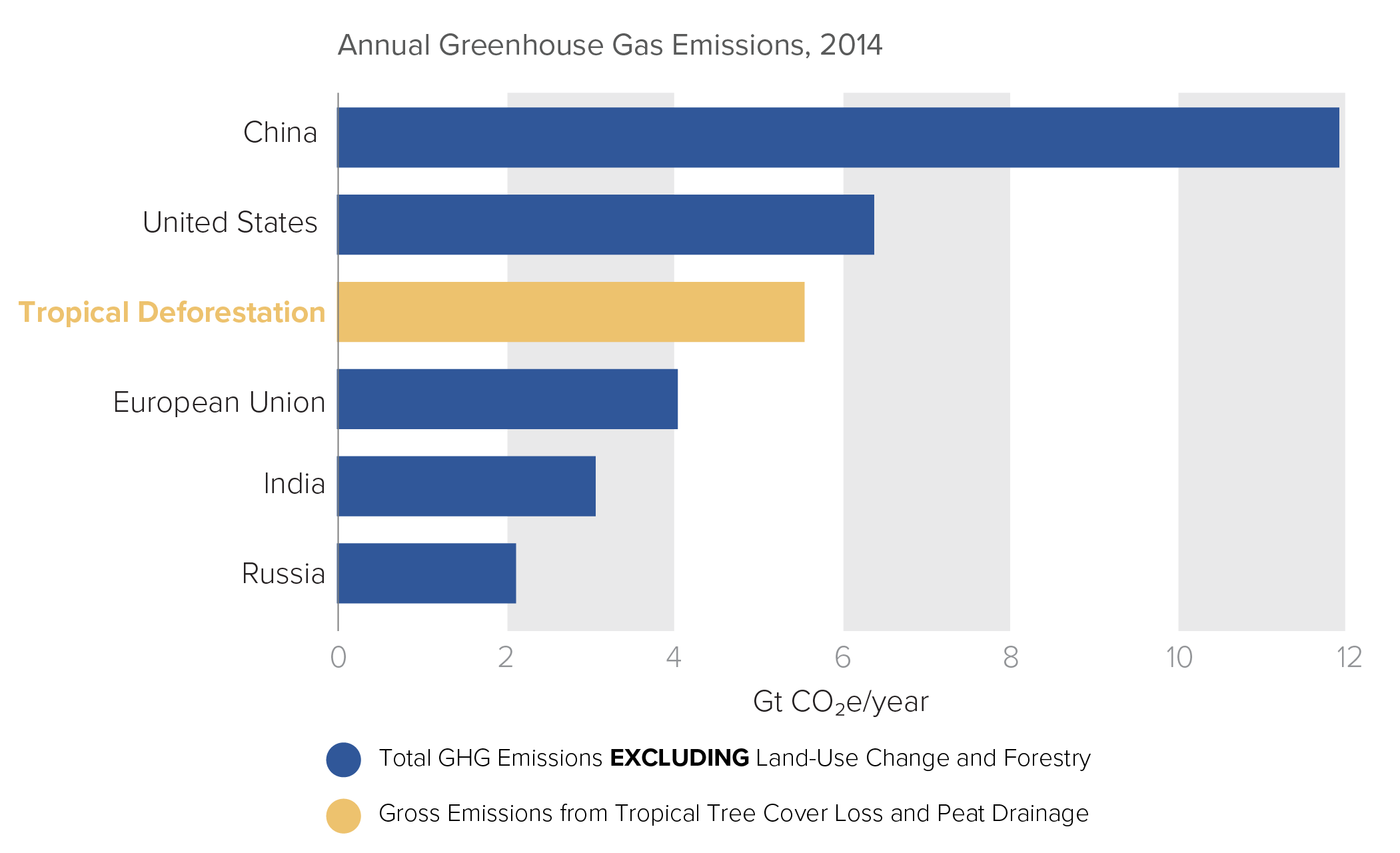

Current trends are disturbing. Despite the scale and urgency of this problem, today’s food and land use system is failing to generate sufficient innovation, investment and attention.3 Forest-related finance for countries with high rates of deforestation accounts for less than 3% of global climate mitigation-related development funding (see Box 32 on Finance for Food and Land Use).4 Global demand for land to grow fuel, feed, and fibre is driving widespread deforestation and forest degradation, with just four commodities – palm oil, soy, beef, and wood products – accounting for more than 40% of tropical deforestation.5 The effect on natural infrastructure is alarming: Biodiversity has declined by more than a quarter in the past 35 years.6 The ramifications of broken food and land use systems on public health are also significant and growing. The convergence of global eating habits on resource-intensive Western-style diets – with the associated commodity consumption driving increased deforestation – is a major contributor to the rise of diet-related, non-communicable diseases that are rapidly becoming a leading cause of human mortality.7 Around 2 billion people are obese or overweight.8 At the same time, persistent inefficiencies and inequalities in the food system continue to leave 815 million people hungry9 while a third of all the food that the world produces is lost or wasted.10 Sticking with our current, unsustainable consumption models will only push these systems further out of balance as the global middle class, with higher incomes and consumption patterns, is expected to number 2.6 billion by 2025, with over 70% of that expansion in emerging markets.11

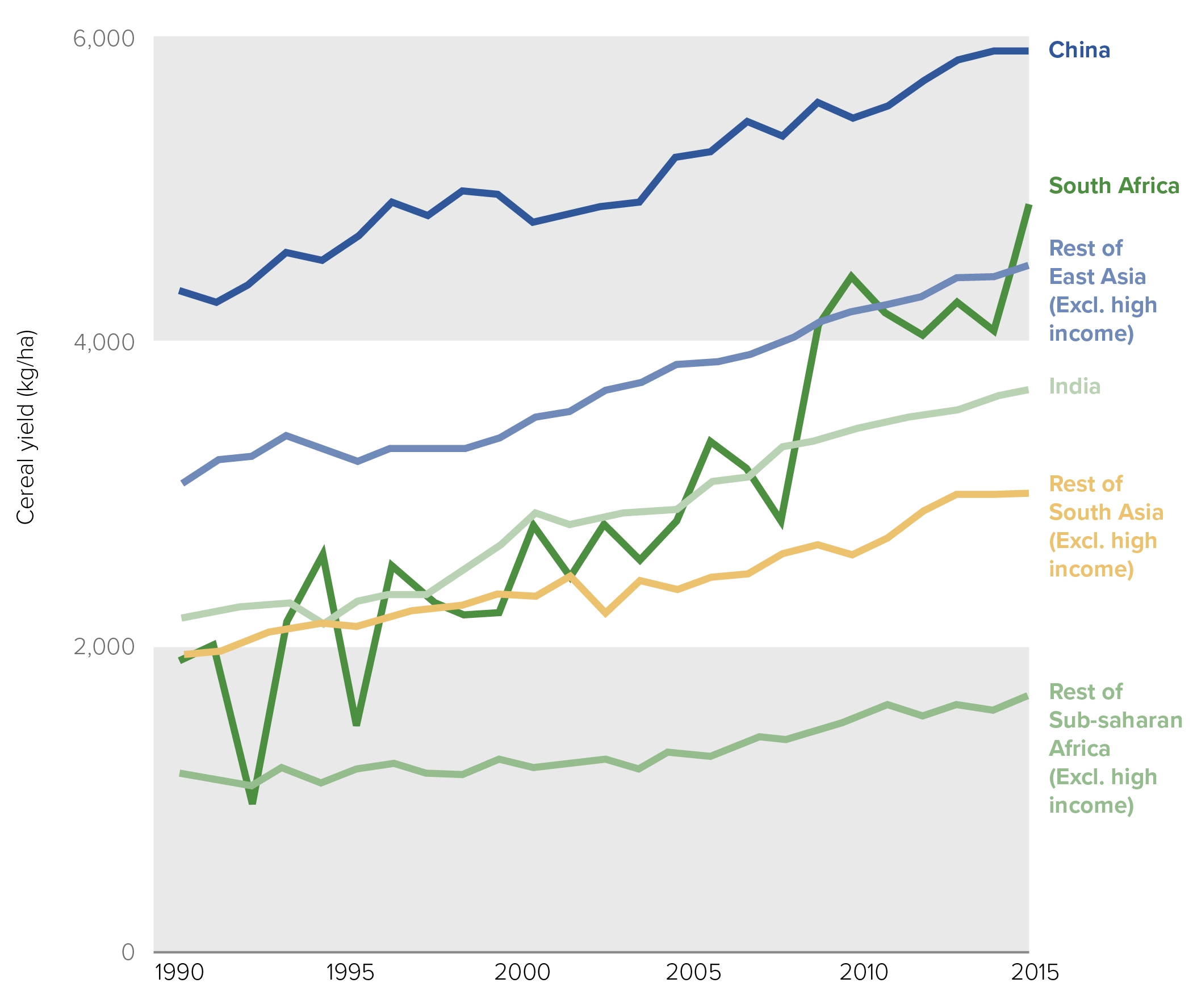

Instead, fixing our broken food and land use system could generate stronger, more resilient and inclusive economic growth, as well as better, more decent work for the several billion people whose livelihoods depend on food, forests and agriculture.12 Reforming agricultural subsidy regimes, worth on average US$519 billion per year (2014-2016), that often lead to inefficient and inequitable economic, development and climate outcomes, could free up valuable public resources with which to achieve a better a food and land use system.13 Halting deforestation could boost the global economy by as much as US$80 billion per year, as well as make it more resilient to a changing climate.14 With a third of the planet’s land degraded,15 a global effort to restore degraded lands either to natural forest or to productive use could generate major economic, employment, and climate gains. In the United States alone, restoration and conservation activities generate an estimated US$3.8 billion a year and currently sustain 126,000 jobs.16 Coupled with a strong commitment to forest and ecosystem protection, sustainably increasing agricultural productivity is essential to meet growing food demand and achieve equitable rural growth. While there have been striking productivity increases in many regions, achieving further productivity gains while reducing agriculture’s climate footprint is possible and needed (see Figure 22).17 Agriculture accounts for almost 70% of total employment in low-income countries worldwide,18 which means that increasing yields and incomes will play a fundamental role in boosting rural livelihoods and ensuring country-wide economic development. Well-managed natural infrastructure can provide sustained economic benefits, which are particularly important for low-income countries, where natural capital constitutes nearly half of the wealth.19 Women also have a vital role to play: If given equitable access to resources, women farmers could help alleviate hunger for 150 million additional people,20 and there are important efforts under way to increase women’s access to knowledge, technology, and resources in the food and land use sector.21

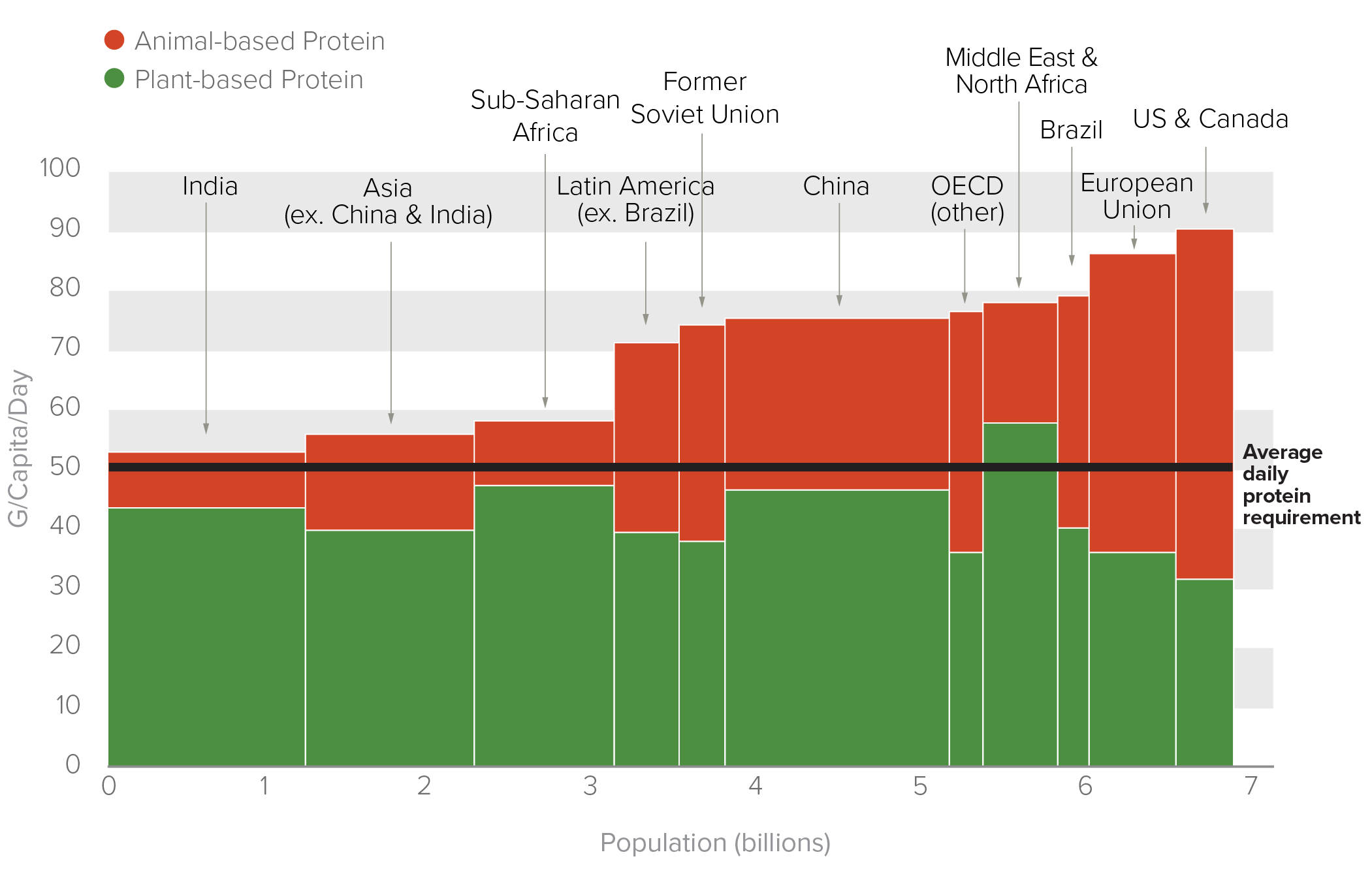

On the public health front, shifting diets from those heavy in animal-based and processed foods – and especially away from beef – towards more plant-based diets could result in global public health benefits, health-related cost savings of almost US$1 trillion per year by 2050,22 as well as significant positive environmental impacts. Reducing food loss and waste is a major economic prize, as well as a moral obligation. Saving just one-quarter of the food currently lost or wasted would be equivalent to the amount of food needed to feed 870 million people annually.23 Reducing food loss and waste also makes good business sense: Recent research of surveyed companies found a median benefit-cost ratio for investments of 14:1.24

In each of these action areas, momentum to reform our food and land use systems is growing, with a number of countries, subnational regions and companies showing the way. In addition, several valuable global collaborative efforts, platforms and sets of champions have emerged to raise ambition and accelerate efforts to reform food and land use systems. Examples of steps in the right direction include the Global Climate Action Summit’s ‘30 x 30 Forests, Food and Land Challenge’: A challenge to non-state actors across all sectors of the economy to take concrete action to ensure better forest and habitat conservation, food production and consumption, and land use, estimating that such action can deliver up to 30% of the ‘climate solutions’ needed by 2030. The Consumer Goods Forum’s (CGF) Zero Net Deforestation Resolution, a resolution by companies to achieve zero net deforestation by 2020 in key commodity sectors, is another. The CGF’s associated partnerships, like the Tropical Forest Alliance 2020, are also helping to turn commitments into action. The New York Declaration on Forests has galvanised a coalition of stakeholders – countries, sub-national governments, companies, indigenous groups, and NGOs – with ambitious global targets to protect forests and end natural forest loss by 2030. The Bonn Challenge, a commitment to restore 150m ha of degraded land globally, created a rallying cry for countries to undertake restoration activities. Building on this, international initiatives AFR100 in Africa and Initiative 20×20 in Latin America are driving significant activity locally. Coalitions and multi-stakeholder partnerships such as the Better Buying Lab and Champions 12.3 are working to accelerate sustainable consumption patterns and efforts to reduce food loss and waste, respectively.

But to truly the fix the food and land use system, piecemeal progress to date must rapidly become a global effort to address these challenges in an integrated and systemic way, at scale. A first-order priority is to close the forest frontier once and for all through a combination of measures including land tenure reform, strengthening protected areas and indigenous peoples’ reserves, effective law enforcement, and measures to ensure that agricultural development takes place on non-forested and degraded lands. Efforts to bring more ‘radical transparency’ to food and land use systems also need to be rapidly scaled. Enhanced transparency, traceability and legality, enabled by satellite imagery and other technologies, is now more feasible than ever before, thanks to tools such as Global Forest Watch and Trase.25 The publication and disclosure of detailed supply chain sourcing data from agribusinesses and traders is required to enhance financial transparency and accelerate meaningful actions by companies and investors.

To scale these and other solutions, smarter and more diverse flows of finance must be innovatively deployed to address food and land use finance gaps and policy incoherence. For example, there are ample opportunities to make smarter use of public finance by reforming agricultural subsidies, implementing ‘full cost accounting’ or price reforms on selected foods, and using blended finance structures. In addition, promising food and land use innovations and new business models – from technologies to lower the cost of planting trees, to lab-grown meats and new forms of alternative proteins, to offering consumers healthier, more plant-based food options (see Box 31) – require further investment and the right policy and investment environments to achieve transformative scale (see Box 32). Governments and the private sector also need to strengthen their actions to reduce food loss and waste and ensure a sustainable, nutritious, and healthy diet for all.