Time to wrap up for the day. And the week. Here's a reminder of the main points:

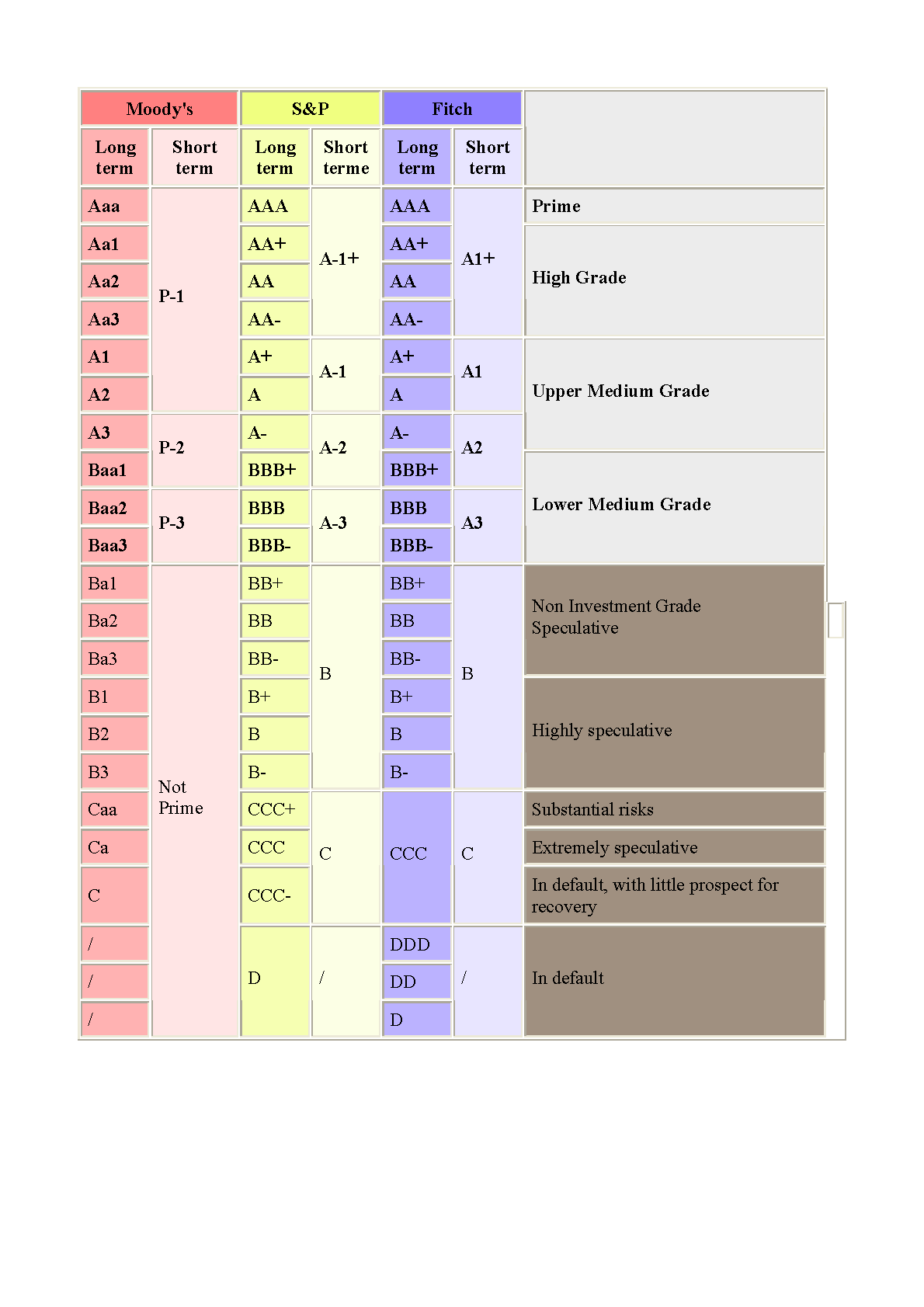

The eurozone's club of AAA nations shrank to three today after S&P stripped the Netherlands of its top credit rating. S&P downgraded the Dutch to AA+, citing weak growth prospects and high households indebtedness.

Finance minister Jeroen Dijsselbloem saidhe was disappointed by the downgrade, but took it seriously, and suggested structural economic reforms would help stimulate growth.

S&P had better news for Cyprus, which was upgraded, and Spain, whose outlook was raised to stable. Here's the analyst reaction.

And inflation also rose, to 0.9%, easing fears the disinflation was setting in.

In Greece, there is confusion tonight over whether the Troika has cancelled its next visit to Athens. Finance minister Yannis Stournaras tells us that it may be postponed....

Greek finance minister: No official Troika cancellation

Over in Athens our correspondent Helena Smith has just spoken to the Greek finance minister himself and can confirm that the upcoming inspection tour by the Troika has not been cancelled - at least officially (see 1.45pm for the rumours).

Helena writes:

Just caught the Greek finance minister Yannis Stournaras in a meeting but ever obliging he agreed to speak for all of a minute and confirm that from the Greek government's perspective, at least, the Troika's visit has not been cancelled. "We are discussing it with them," he told me. "It's definitely not been cancelled, maybe there will be a postponement for a couple of days but it definitely has not been cancelled," Stournaras insisted.

Behind the scenes there is much speculation that the threat of a no-show is yet another negotiating ploy to pile the pressure on Greece and finally get it to implement some of its long overdue "prior actions."

Inspectors have been alarmed to see that many public sector employees moved into a "mobility scheme" as part of efforts to trim the boated public sector have still not seen their salaries reduced to 75 percent of their original paychecks apparently because of resistance from the government's junior socialist partner Pasok, Other prior actions include the closure of Greece's loss-making defence industry and privatisation of the water Board EYDAP.

If mission heads do not return it will be the third time in the space of a single review that they have left Athens empty handed. "We want to avoid that at all costs," said another Greek official accepting that tensions between the two were unusually high.

"Right now I can confirm that we are preparing a file to send to our lenders outlining all our positions on all the outstanding issues. They will have it tonight. Don't forget, this is a negotiation."

Sterling vs dollar for last five years. Photograph: Thomson Reuters Photograph: Thomson Reuters

The pound has hit its highest level since August 2011.

Sterling traded at $1.6383 against the US dollar (the 'Cable' trade), a whisker above the highest level of 2013, set at the start of January.

It has been rising in recent days, on predictions that the strenth of the UK economy will prompt the Bank of England to tighten policy earlier that is officially suggesting.

Political analyst Alberto Nardelli flags up some opinion poll data from Italy today, showing that public support for Silvio Berlusconi actually rose this week.

#Italy IXE poll: trust in Silvio Berlusconi +6 from last week (Renzi stable, Letta -4, Grillo -1, Alfano -2) pic.twitter.com/v3oUt9K8JS

It's a sign that Berlusconi's political influence could be undimmed by his expulsion from the Senate this week....

He does now lack parliamentary immunity, though, as was shown this morning when an Italian court accused the former prime minister of bribing witnesses to give false testimony in a trial linked to the case in which he has been convicted for paying for sex with a minor.

Berlusconi's lawyers, Niccolo Ghedini and Piero Longo, who were also accused of inducing false testimony in the case. They have strongly denied the charges as "totally disconnected from reality and from the facts".

Black Friday has also turned nasty in Britain, where ASDA (part of WalMart) has introduced the concept today.

As my colleague Sarah Butler reports:

Shoppers took to the social media site Twitter to describe early morning queues and fights. A woman in Merseyside was reportedly taken to hospital in the morning after being assaulted in a queue outside an Asda store. A man was arrested in Bristol after another fracas.

More here, including a dramatic picture of the arrest:

Black Friday isn't just about rampant American consumerism. Well, not quite. It's also an opportunity for US workers to protest about their conditions.

Thousands of demonstrations are expected at WalMart stores across the country, as the OUR Walmart group pushes the retail giant to commit to paying higher wages to its staff.

There are also reports of shoppers trading blows as they battle to grab the best bargains.

Over on Wall Street, traders have staggered back to their desks after yesterday's Thanksgiving gorge-a-thon, and found the appetite for a little trading.

The Dow Jones index is up 50 points in early trading at 16,147, adding 0.3% to Wednesday's record close.

Microsoft is the biggest riser, up 1.2% this morning as American shoppers battle to get their hands on the latest electronics kit in the Black Friday sales. And this year, some UK shops are taking part too.

A well-placed Greek finance ministry official who is in daily contact with Yannis Stournaras, the technocrat national economy minister, said there was still "a possibility" that international inspectors representing the country's "troika" of lenders would visit Greece next week.

From Athens, Helena Smith writes:

"I don't care what Reuters is saying" he said, referring to the agency's report that the visit had been postponed putting a wrench in negotiations being completed before the next euro group meeting on December 9th.

"We never had a concrete date for the visit even when the media was saying the [EU/ECB and IMF] representatives would be back on Monday.

"And we still don't have a date. There is still most definitely a possibility that they will return," he said.

Regular readers will recall that Stournaras, and pirme minister Antonis Samaras, have both said in recent days that they want negotiations wrapped up by the end of the year before Greece assumes the rotating EU presidency in January.

EU and IMF lenders backing Greece have called off a planned visit to Athens next week, a move that may delay the payment of further loans to the country, officials told Reuters on Friday.

The visit by the "troika"of the the European Central Bank, International Monetary Fund and European Commission was cancelled because Greece has failed to carry out certain reforms promised in its aid programme, the officials said.

The inspectors had been due to assess Greece's progress ahead of a meeting of euro zone finance ministers on Dec. 9.

Asked if the cancelled visit meant it might not be possible to approve the next tranche of aid to Greece, one official responded by email: "Correct".

A spokesman for the European Commission said discussions with Athens would continue. "We have not yet taken a decision on precisely when the mission will return," he said.

EU Says No Decision Taken on Troika Mission’s Return to Greece

Reuters is reporting that officials from Greece's troika of lenders have cancelled plans to return to Athens next week to discuss its bailout programme.

RTRS - EU-IMF INSPECTORS HAVE CALLED OFF VISIT TO GREECE PLANNED FOR NEXT WEEK DUE TO ATHENS' FAILURE TO MEET COMMITMENTS - OFFICIALS

We're looking into it.....

It would mean there's no chance of getting Greece's next aid payment agreed at the upcoming meeting of eurozone finance ministers on Monday 9th December.

Local media citing #Greece MoF source indicate it has not yet been decided whether #troika will return to Athens on December 2. #economy

Bankers continue to cream off too much money for their own senior staff rather than serving the economy, campaigners for a financial transaction tax are claiming.

Simon Chouffot, spokesperson for the Robin Hood Tax campaign, said:

"It's outrageous that five scandal-ridden years after causing the biggest crash in a generation bankers are still receiving such bloated rewards.

"These pay packets are more than 32 times the average salary in the UK. If the banks can afford to dole out such excessive sums they can also afford to contribute more for the damage they have caused to society.

"The fact that they are already trying to wriggle out of the incoming bonus cap shows more fundamental change is needed to bring financial sector excess back under control."

The number of bankers based in the EU who earn at least €1m per year rose by 11% in 2012. And three quarters of them worked in Britain.

A report from the European Banking Authority this morning showed that 3,529 bankers were paid at least €1m in 2012, with 2,714 based in the UK -- most, presumably, in the City of London and Canary Wharf.

The average pay of those 2,714 UK bankers was almost €2m last year, which critics are likely see as a sign that banking remuneration remains too high. It's a 35% increase on last year (Sky News has more details)

Bonuses dwarfed basic pay last year. In the UK, bankers earning at least €1m received a total of €1.12bn in fixed pay, and shared another €4.169bn in variable remuneration. That means bonuses made up 79% of total pay, or were 390% as much as basic pay.

That shows that the EU bonus cap -- at 100% of basic salary, or 200% if shareholders agree -- would have a big effect on City pay packets. But would take-home pay fall, or basic pay simply rise?

Here's how the UK figures broke down (showing that most top earners were investment bankers, although many asset management and retail bankers did pretty damn well too)

Photograph: EBA Photograph: EBA

The figures are being gathered as part of Brussels' attempt to ensure that bank pay is designed to ensure "sound and effective management", and to encourage "prudent long-term risk taking in the EU banking sector".

The figures underline how much of the EU's financial sector contained in Britain. In German, just 212 bankers received over €1m, followed by France (177), Italy (109) and Spain (100). Both Greece and Slovakia reported just one seven-figure banker each.

The first fall in euro zone unemployment in almost three years coupled with rising prices gave fresh momentum to an economic recovery, but a growing rift between the bloc's haves and have-nots continued to widen.

The improvement is a welcome sign that the euro zone's rebound is picking up steam, more than five years after a financial crisis erupted that forced five countries from Cyprus to Spain to seek emergency aid from their neighbours.

The jobless rate in October fell to 12.%, the first fall since February 2011, the European Union's statistics office Eurostat said on Friday.

That was slightly better than the 12.2% that economists forecast but it belies a wide disparity across the 17 countries using the currency.

While just 5% of Austrians are unemployed, 27% of Greeks and Spaniards are without a job. In total, 19 million people are out of work.

Consumer prices in the euro zone rose by 0.9% in November, higher than the 0.8% forecast in a Reuters poll of economists.

The annual inflation rate was also up from the 0.7% level in October, a sharp drop from September that surprised policymakers and raised concerns about the threat of deflation.Energy prices fell in November, but the rising pace of food inflation pulled up the overall reading.

Still, there are wide divergences across the bloc, with Greece, Cyprus and Ireland suffering deflation in October.

Incidentally, the record youth unemployment rate doesn't take into account young people who are economically inactive. It's a measure of those under 25 who are looking for work, compared to the total youth labour force.

The raw fact is that 3.577m people aged 15-24 in the eurozone were looking for work in October, 15,000 more than a year ago, out of a youth labour force of over 14 million.

EU and eurozone youth unemployment Photograph: /Eurostat/Markit Photograph: Eurostat/Markit

The youth unemployment rate in the eurozone has climbed to a new record high.

The news takes the shine off the the first drop in the overall eurozone jobless rate for almost three years announced this morning (see earlier post).

Eurostat reported that the unemployment rate for those under 25 in the euroarea rose to 24.4% in October, the highest level it has ever reported (the press office confirm). It was 24.3% in September 2013, and 23.7% a year ago.

Rates are particularly high in the Southern European countries that have been hit hardest in the eurozone crisis.

Spain's youth unemployment rate climbed to 57.4% in October, up from 56.8% in September.

Italy's youth unemployment rate rose to 41.2%, from 40.5% the previous month.

In Portugal, it rose to 36.5% from 36.2%.

New data for Greece wasn't released - but in August its youth unemployment rate was 58%.

The picture is hardly better in the wider European Union, where the youth unemployment rate was measured at 23.7% in October.

This graph shows how unemployment in the eurozone rose to record levels through the crisis and recession, before the small drop in the jobless rate to 12.1% in October.

The eurozone unemployment rate has fallen, offering the hope that the region's long jobless crisis could finally be easing.

But the rates of youth unemployment remain painfully high, as Europe's lost generation struggle to find work.

The unemployment rate in the euro area fell to 12.1%in October, Eurostat reported, down from 12.2% in September. During the month, the number of people unemployed fell by 61,000 in the euro area, to 19.298 million.

For the wider EU, the unemployment rate was unchanged at 10.9%.

The youth unemployment rate in the European Union was recorded at 23.7% -- a year ago it was 23.3%.

Eurostat also rounded up the stark difference in national unemployment rates:

Among the Member States, the lowest unemployment rates were recorded in Austria (4.8%), Germany (5.2%) and Luxembourg (5.9%), and the highest in Greece (27.3% in August 2013) and Spain (26.7%).

Compared with a year ago, the unemployment rate increased in half of the Member States and fell in half.

And the Netherlands, hit by a downgrade this morning, saw one of the biggest annual rises.

Eurostat again:

The highest increases were registered in Cyprus (13.2% to 17.0%), Greece (25.5% to 27.3% between August 2012 and August 2013) and the Netherlands (5.5% to 7.0%). The largest decreases were observed in Latvia (14.0% to 11.9% between the third quarters of 2012 and 2013), Ireland (14.5% to 12.6%) and Lithuania (13.0% to 11.1%).

JUST IN: Inflation in the euro area rose in November.

The Consumer Prices Index rose by 0.9% annually this month, an increase on October's 0.7%, which will calm some fears that the region is sliding into deflation. It's still some way from the ECB's target of just below 2%, though.

In the UK, mortgage approval levels have hit their highest level since the financial crisis began.

Mortgage approvals rose to 67,701 in October, from 66,891 the previous month.

That rather vindicates that Bank of England's decision yesterday to stop letting banks use its Funding for Lending scheme for household loans. Although we're still not close to pre-crisis levels of mortgage approvals:

Note that while mortgage approvals are at the highest level since 2008, they're hardly close to pre-crisis peak pic.twitter.com/RUjsfGrK2o

Dutch finance minister: we take downgrade seriously

Photograph: CNBC Photograph: CNBC

Netherlands finance minister, Jeroen Dijsselbloem, has said he's disappointed by the loss of the country's AAA rating, and takes S&P's decision "seriously".

Speaking to CNBC, Dijsselbloem said the Dutch labour market, housing market, and pensions system are "the main factors holding back our economic recovery". He pledged to make structural reforms to ensure the recovery "picks up in strength".

Asked for his ''emotional response" to the downgrade, Dijsselbloem replied:

I don't have an emotional response. I take these ratings seriously because the market takes them seriously.

It just confirms the need for us to push forward some of these reforms so that we can get bigger and better growth figures.

He added that Fitch and Moody's recently affirmed the Netherlands AAA status, "and now S&P has downgraded us to AA+".

I'm disappointed by that fact, but I take it seriously because these are serious agencies which are take seriously by the markets.

The president of Cyprus, Nicos Anastasiades, has welcomed S&P's decision to upgrade his country's credit rating.

He tweets that the upgrade is the result of the "consistent and decisive policy" that his government has followed since accepting a €10bn bailout programme that included tough capital controls - restricting how much money people can take out of the bank.

Anastasiades added that the upgrade should held rebuild confidence in Cyprus's economy, and pledged to maintain disciplined and prudent policies to tackle the challenges ahead.

Η αναβάθμιση του Standard and Poorʼs, αποτελεί το αποτέλεσμα της συνεπούς κ αποφασιστικής πολιτικής που ακολουθούμε τους τελευταίους 8 μήνες

There was a time when a eurozone credit rating downgrade would shake the markets.

Not today, though -- stock markets are calm across Europe. The FTSEurofirst 300, which includes the biggest stocks across the region, is flat after hitting a five-year closing high last night. Even the Amsterdam market is calm (up 0.04%)

Investors do have good news to digest too -- the upgrade of Cyprus (suggesting less danger of a default), and the raising of Spain's outlook to stable:

Upgrade of Cyprus to B- is the surprise move from S&P this morning. Netherlands/Spain less of a shock.

One of the Netherlands' many problems right now is negative equity after it suffered a nasty housing crash (there's a good feature on the BBC)

By last summer, one in four houses were worth less than the mortgages taken out to pay for them. This has left the banks nursing bad loans and prevented people moving house; hurting the economy and slowing its exit from recession.

Consumer spending is also sliding -- with retail sales slumping by 6.1% year-on-year in September.

As a member of the eurozone's Northern core, the loss of the AAA rating must sting the Netherlands - (even though they clung on about two years longer than France managed).

That core, though, looks rather less healthy than it once did. As Deutsche Bank put it in August:

The Netherlands is more akin to a 'peripheral', with dramatically rising unemployment, spiking business failures and economic confidence detaching from the AAA peer group and moving to crisis country levels.

Good morning, and welcome to our rolling coverage of events across the world economy, the financial markets, the eurozone and the business world.

The Netherlands has lost its AAA credit rating, whittling down the number of eurozone members with a top-notch credit rating to just three, in the latest reminder that the economic problems in the region are not over.

S&P downgraded the Dutch credit rating early this morning by one notch to AA+, saying that the country's weak growth prospects were incompatible with the prized triple-A rating

But it also upgraded Cyprus, and raised Spain's outlook in recognition of progress made by Madrid.

S&P warned that the Dutch economy will have shrank by 1.2% this year (it just clawed its way out of recession), and only sees growth of 0.5% in 2014.

We do not anticipate that real economic output will surpass 2008 levels before 2017, and believe that the strong contribution of net exports to growth has not been enough to offset a weak domestic economy

The downgrade reflects our opinion that The Netherlands’ growth prospects are now weaker than we had previously anticipated, and the real GDP per capita trend growth rate is persistently lower than that of peers.

While credit rating agencies remain discredited in some quarters following their failure to spot the financial crisis bubbling away, the downgrade will still be a blow to the Netherlands' government. It is pushing austerity measures through in the face of weak consumer spending and a house price crash.

It means Germany, Luxembourg and Finland are the only countries left with a AAA rating with the 'Big Three agencies.

Moody's and Fitch still rate the Netherlands as AAA, but with a negative outlook.

S&P upgraded Cyprus, though, from CCC+ to B-. It said that the risk of default has eased since the country slumped into an IMF-led bailout this spring.

It said:

The stable outlook reflects our view of the implementation risks that remain as the end of the three-year European Commission, International Monetary Fund, and European Central Bank program approaches, balanced against the upside potential we see coming from Cyprus' economy.

S&P also has cheerier news for Spain -- it raised its outlook from negative to stable, removing the threat of a downgrade. The agency cited the gradual return of growth to Spain, adding:

Other credit metrics are stabilizing, in our view, due to budgetary and structural reforms, coupled with supportive eurozone policies.

The effectiveness of those eurozone policies will become clearer through the day, as new unemployment and inflation data is released at 10am GMT.

Reaction to follow, along with other developments through the day.

{kind=link}

Comments (…)

Sign in or create your Guardian account to join the discussion