MOL Triumph is the world’s largest container ship. In line with the eco-sailing initiative of MOL, the new 20,000 TEU-class container ship is equipped with various advanced energy-saving technologies, such as low friction underwater paint, high efficiency propeller and rudder. It has an optimized fine hull form that can further reduce fuel consumption and CO2 emissions, per container moved, by about 25-30 percent when compared to 14,000 TEU-class container ships.

Photo courtesy Lloyd’s Register

As CEO of Lloyd’s Register I often reflect on how our role has evolved over our 257-year history.

When we were founded in 1760 our role was to protect ships and their crews from the harsh marine environment. Although that role continues, we also play a major part in protecting the environment from ships and their crews.

The greenhouse gas (GHG) emissions of shipping are a consequence of the carbon intensity of shipping’s energy supply, the energy efficiency of shipping and the demand for shipping. The Paris Agreement on climate change confirmed that it was not a question of whether climate change should be addressed but a question of how, and it is clear that everyone will have to contribute.

Shipping is arguably the most carbon-efficient mode of commercial transport and is fundamental to the functioning of the global economy. International trade, the transport of bulk raw materials and the import/export of everyday food and goods would simply not be possible without maritime transportation.

Global shipping, which transports around 90 percent of world trade, currently accounts for 2.3 percent of the world’s total GHG emissions, compared to 2.8 percent in 2007. Total shipping emissions have been reduced by more than 10 percent during the same period. However, there will be no space in the carbon budget to allow even the emissions of shipping (currently approximately 1 gigaton per annum) to be ignored.

The international shipping industry, through the International Maritime Organization, is firmly committed to playing its part in reducing emissions of CO2 and other greenhouse gases. The challenge the industry faces in reaching an absolute target is that shipping is the servant of world trade. The total emissions of shipping, as a sector, will therefore be determined, to a significant extent, by the expected long-term growth of the world economy (and population) between now and 2050.

There are few certainties about the future of ship design and operation, and, by association, the wider system within which ships operate (ports, bunker suppliers and supply chains, trade, freight handling and logistics, etc.). One important uncertainty is how the regulatory landscape for the control of shipping’s GHG emissions will unfold: Which incentives and levers might become important drivers of investment and operational decisions in shipping and when?

The designers, owners and financiers of a ship designed today and launched around 2020 would probably like that ship to retain its commercial viability for several decades. How can we best think that through?

Low Carbon Pathways 2050—a joint study by Lloyd’s Register and Shipping in Changing Climates—sets the detail of the regulatory debates to one side and answers the question: Given the current best available evidence, what is a reasonable estimate of how shipping might be required to change and what does this look like?

Consistent with the Paris Agreement, the report gives particular focus on the technological and operational specifications of the global fleet and how these may change in relation to a given rate of decarbonization.

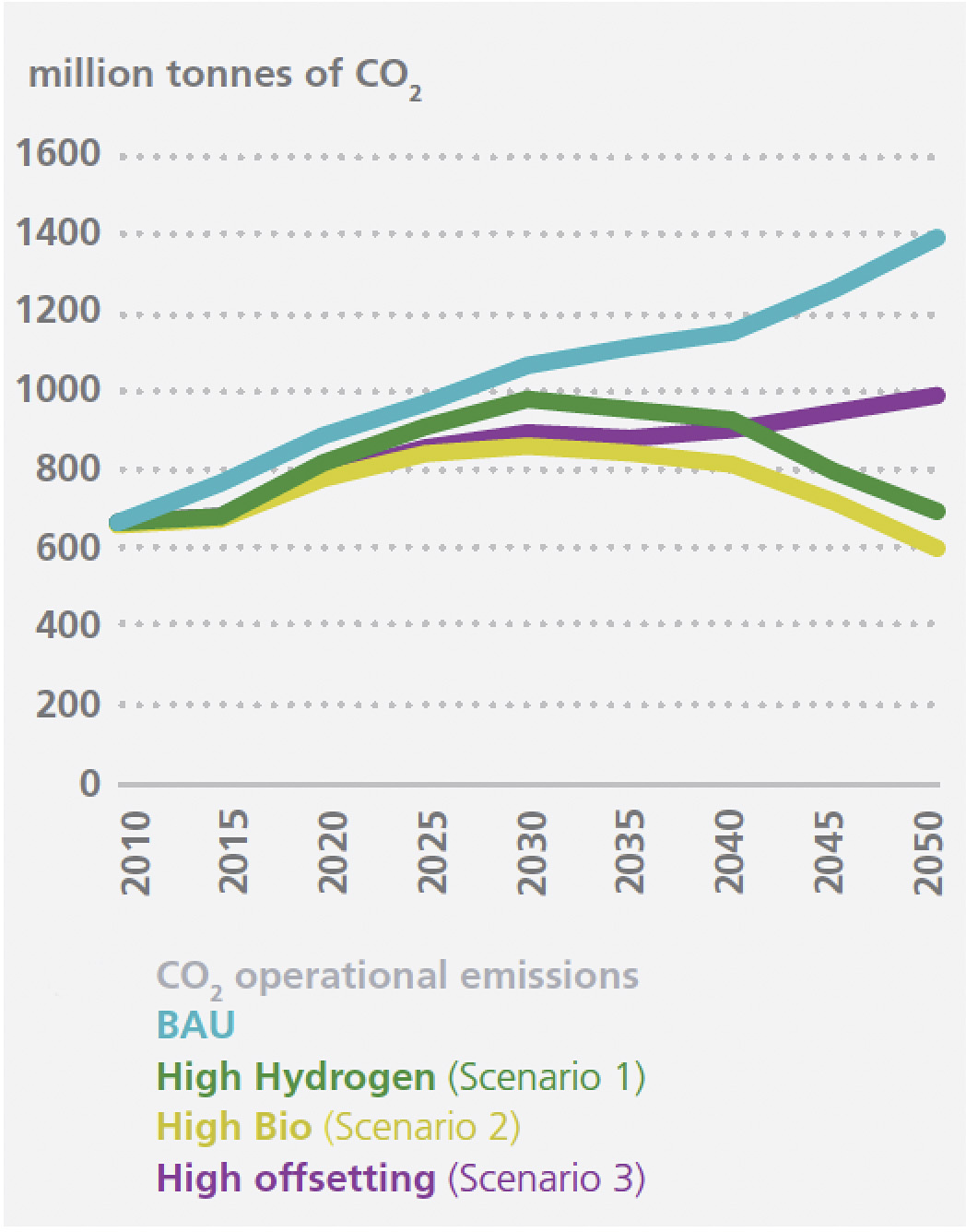

Three future scenarios for this initial study for the period 2015–2050 were identified to demonstrate varying options for decarbonization. The first, High Hydrogen, considers the availability of hydrogen, which is used in fuel cell technology, to demonstrate what can be achieved through technology and innovation. The second, High Bio, assumes a mid-range market penetration of biofuels in the shipping industry, and the third, High Offsetting, considers the impact of a market-based mechanism. These three future scenarios are compared to a business-as-usual (BAU) scenario with existing regulatory commitments.

The total operational CO2 emission trajectories are presented in this for the ship types included in this analysis (wet and dry bulk and container shipping); these are not inclusive of any absolute reduction of emissions achieved through offsetting. The Business As Usual scenario shows an increase in CO2 emissions. In scenarios 1 and 2, by 2050, shipping net emissions decrease relative to the BAU scenario by approximately 50%. Both scenarios’ emissions peak in 2030 followed by a steadily increasing rate of decarbonization. In scenario 3, operational emissions continue to increase, with the 33 Gt carbon budget being achieved through the use of offsets. Source: Lloyd’s Register, Low Carbon Pathways 2050

The specifics of how shipping might change vary depending on the assumptions made. The scenarios cannot envisage the role that innovation might play in any transition, as they are limited to the mix of technologies defined as input assumptions. However, we can show that different scenarios have different consequences for the technology mix of the industry and that further work is needed if shipping is to manage its transition while maximizing resilience and minimizing the risks of technological obsolescence. Innovation can produce lower cost alternatives as well as help to reduce the cost or increase the performance of technologies that have already been identified.

However, one key finding is that most of the pathways will require a substitute for fossil fuel, because energy efficiency improvements alone will not be sufficient in the medium to longer term. Energy storage in batteries and renewable energy sources (wind and solar) will undoubtedly have important roles to play but are still likely to leave a requirement for a liquid fuel source.

The results of the report show that, in the scenarios considered, shipping is likely to need to start its decarbonization imminently, and that the associated changes will be fundamental and require a lot of further work and development to minimize disruption.

This is important because, in all parts of the global economy, not just shipping, decarbonization starts with the low-hanging fruit. As stringency increases over time, increasingly high-cost mitigation steps are required. Therefore, while it might be tempting (given the timeframe in play) to try and ignore the cumulative nature and scale of shipping’s decarbonization challenge for a bit longer, the report shows that this is not a sound strategy. The later we leave decarbonization, the more rapid and potentially disruptive it will be for shipping.

Following this initial study, we are convening industry roundtable discussions on the findings of the report and are facilitating the development of future possible scenarios in collaboration with the industry to create and share knowledge and tools that can contribute to reducing GHGs from shipping.

There are many issues to debate as the industry tries to consider what the strategy might be for handling the simultaneously inevitable and uncertain changes ahead. What is clear is that any future regulation needs to provide the right incentive to drive the change needed, and we hope that business strategies and consistent policies can be combined to reduce shipping emissions.